You may be considered for a hardship variation if:

*This is not a complete list and other causes of hardship may be considered by your lender.

Possible variations to your credit contact can include:

You may also need to show how you will make up the missed repayments. This may include:

1

Read our Hardship Variation Fact sheet and watch our video to familiarise yourself with hardship variations.

2

For assistance in preparing your hardship variation application you may wish to use our online Auto-Letter form, or alternatively, see our Sample Hardship Variation Letter.

3

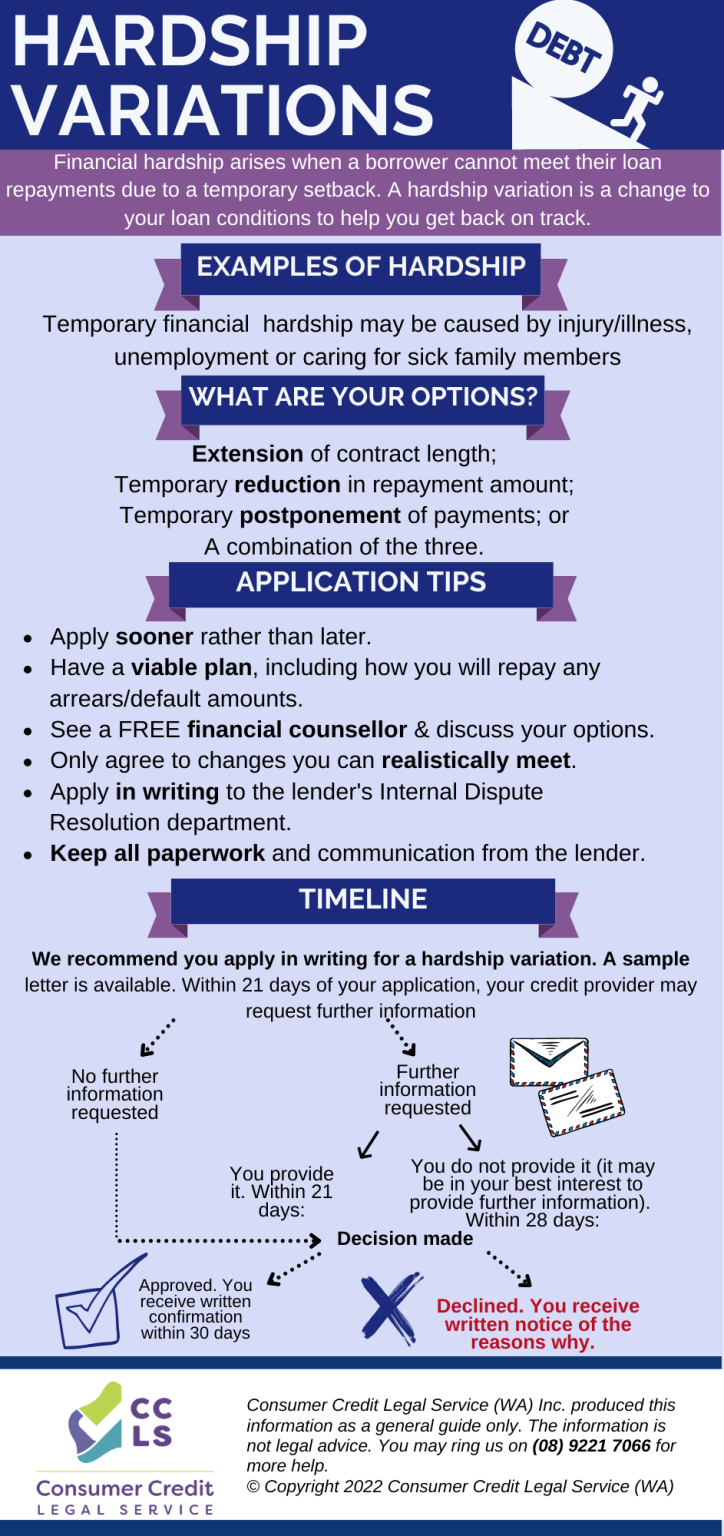

The lender must advise you whether your request for variation has been accepted or rejected within 21 days. They may also ask you for further information.

If you do not receive a response within 21 days or at all then you may wish to lodge a dispute with AFCA.

4

If your hardship variation application is accepted, the credit provider – within 30 days of accepting the variation – must give written notice of the conditions of postponement.*

This notice must also specify the consequences of not complying with these conditions.

If you fail to comply, the credit provider may seek to recover the debt from you.

If your request is unreasonably rejected, you may wish to lodge a dispute with AFCA.

Information on our website is provided for information only and is not legal advice. If you would like legal advice, please message us using the form below for a confidential discussion, or scroll down to see other ways to reach us.

If you would like further advice or have a received a court document, please message us using the form below for a confidential discussion, or scroll down to see other ways to reach us.

{kind=link}