Buying a new or second-hand car can be a daunting experience. When buying a vehicle, there is an added worry of buying a lemon car. CCLS have assisted many clients who have reportedly purchased a lemon. The hassle in navigating such a negative situation can be avoided by following some simple steps:

It is also important to understand all one off and ongoing expenses before you buy a motor vehicle. More information on these expenses are outlined on the MoneySmart website and within our Buying your first car factsheet and infographic.

The PPSR is an online database that records whether the car you want to buy has been:

If the car has been used as security for a loan, the lender with the security-interest recorded on the PPSR may repossess the car from you if they do not receive payment for the loan owed.

For more information on the PPSR, and how to use it, visit the PPSR website or call our advice line on (08) 9221 7066.

A PPSR search should only cost you $2 and could save you thousands as well as emotional stress. Ensure you are using the official PPSR site to avoid unnecessary charges.

You can check for outstanding payments and fines by looking up the number plate via the Department of Transport website.

Verify whether regular services have been conducted and identify any pending maintenance tasks for uncompleted items.

Use this drive to understand how the car drives, if all the functions (steering, breaking, indicators, mirrors, seat adjustment, lights, windows, wipers, sound, heating and cooling, reversing cameras and navigation) all work as they should and if there are signs of any visible damage/issues with the vehicle.

If possible, have a mechanic inspect the vehicle and check for any issues or odometer tampering. Review the warranty if any and note any items you want to have fixed before purchase and if signing a contract, ensure these terms are noted in writing on the contract.

Consumer Protection WA has created an easy-to-follow checklist for buying cars along with a webpage with more information. Follow this checklist when buying a car to avoid being taken for a ride.

https://vimeo.com/630599035

View Infographic

If you are borrowing money to purchase a car, you will usually be entering into two separate contracts:

• A purchase contract with the dealership to buy the car; and

• A car loan credit contract with a lender.

If you are applying for finance to complete your purchase, it is important to make sure that the purchase contract is marked ‘subject to finance’. This will ensure that the contract does not become binding until you obtain finance and allows you to terminate the contract if you are unsuccessful in getting finance.

However, you must also have made reasonable attempts to get finance. We would consider applying to 2 or 3 different lenders will be reasonable. Further, you do not have to accept an offer for finance that is not financially suitable or does not meet your requirements of objectives for the loan. See our factsheet about ending a contract to buy goods or services which is “subject to finance”.

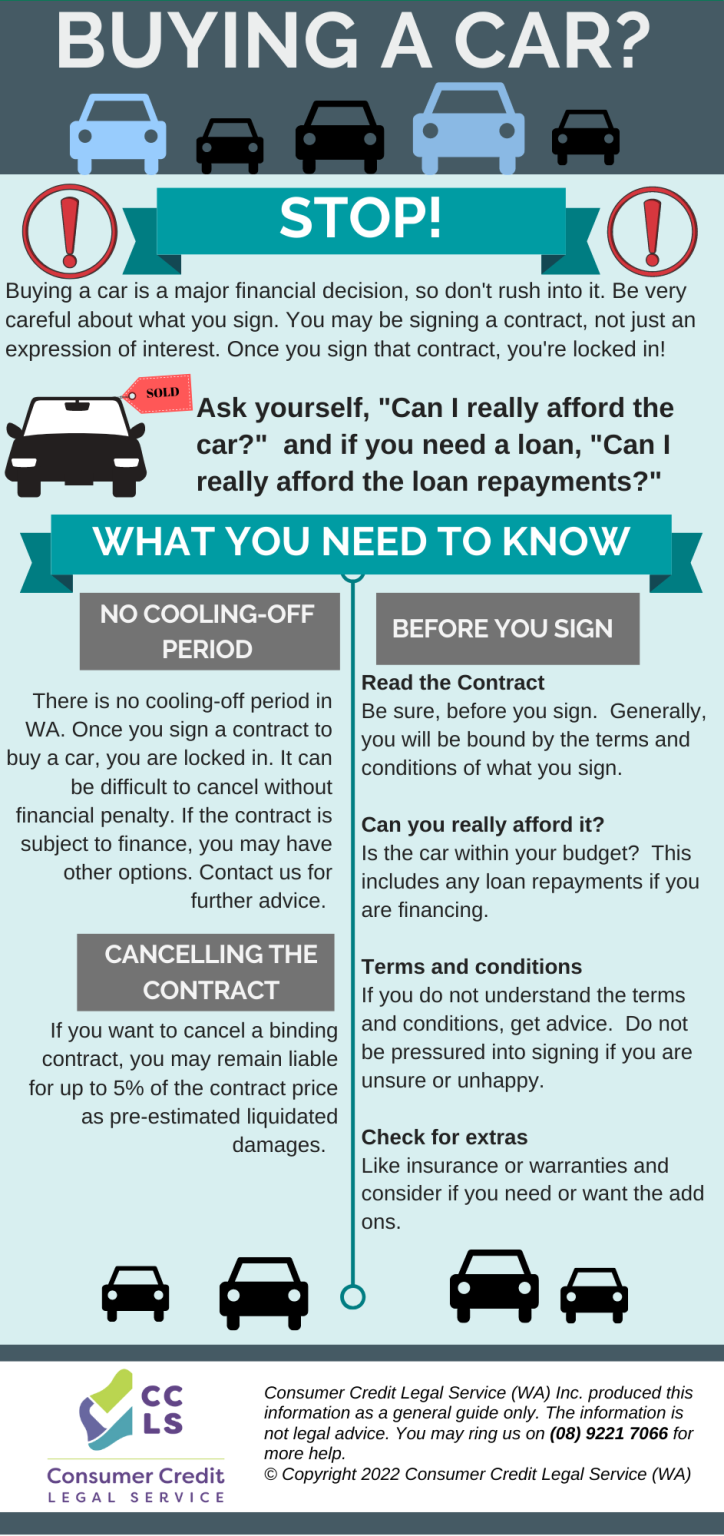

In Western Australia, there is presently no designated ‘cooling-off’ period for vehicle contracts. However, you retain the right to withdraw from a contract at any point before the dealer officially signs it. Should you find the need to cancel a vehicle contract after the dealer’s signature, the dealer might request payment for ‘pre-estimated liquidated damages’ (PELD).

It’s important to note that the maximum allowable PELD charge is capped at five percent of the total purchase price, however, the dealership is not allowed to automatically charge the full five percent. Any PELD charged needs to be a genuine and reasonable assessment of the losses the dealership has suffered because of the sale not going ahead.

Don’t be pressured into buying extra add-on insurances and warranties that are not good value or do not provide you with any benefit above the statutory rights you have anyway under the ACL. The “deferred sales model” means that the dealership cannot sell you add-on insurance within 4 days of the car purchase to provide sufficient time to make a more informed decision and reduce the number of unnecessary purchases.

If you are purchasing your car from a dealership the Australian Consumer Law (ACL) applies and you have consumer guarantees regarding the quality of your purchase. You may be entitled to repair, refund, or replacement in certain circumstances if your consumer guarantees are breached. Your consumer guarantees cannot be contracted out of and apply independently of any add on insurances or warranties. Please see our fact sheet on Consumer Guarantees.

If you would like advice on your consumer rights when buying a motor vehicle, please message us using the form below for a confidential discussion or scroll down to see other ways to reach us.

Skip to content Skip to content

Skip to content

{kind=link}