If you have an outstanding debt with a credit provider, you may be contacted by a debt collector.

If a debt collector contacts you, you should ask:

This is important because it will determine who you may negotiate with and where you may direct your complaints.

The Debt Collection Guidelines encourage debt collectors to work with you and to adopt a flexible and realistic approach to negotiating repayment arrangements. This includes making reasonable allowances for living expenses, consideration for people with low incomes and ensuring payment arrangements are sustainable.

Possible negotiations may include:

Financial Counsellors may assist with such negotiations or with managing debts generally.

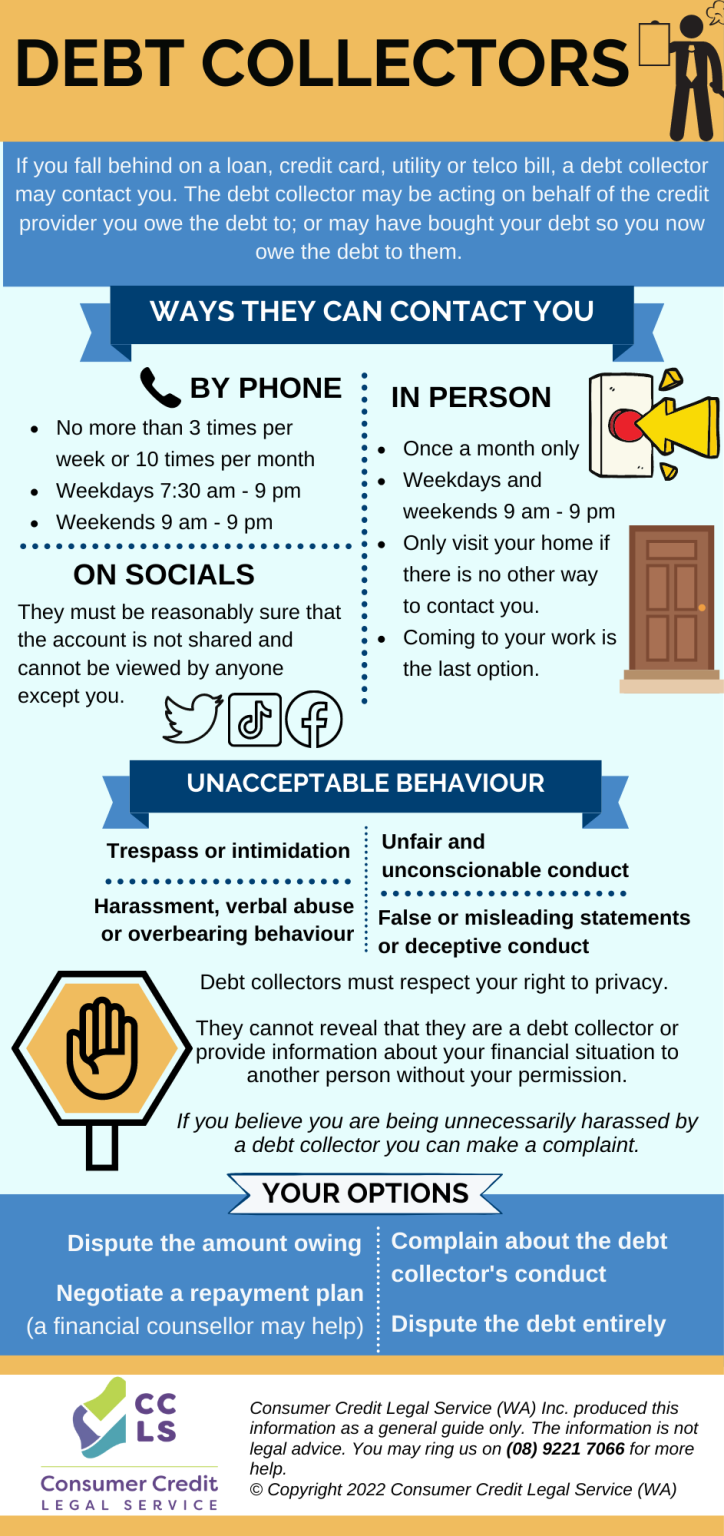

The conduct of creditors and all debt collectors is regulated by the Debt Collection Guideline. Under this Guideline, creditors and debt collectors cannot do certain things when pursuing payment of a debt.

This involves limitations on the location, hours and frequency of contact and the communications to third parties (including children).

Behaviour by the debt collectors should also not be threatening, intimidating or abusive. They should not misrepresent or mislead you by making false statements (for example, regarding the consequences for non-payment).

For more information on what debt collectors can and cannot do, see our factsheet.

If you feel that you are being harassed or unfairly treated by a debt collector, you may be able to make a complaint against the debt collector. To assist you in making a complaint to a debt collector, see our sample letter.

If it has been six years since you have last acknowledged or made a payment towards a debt and there has not been a court judgment against you, the debt may be statute-barred.

This means that the debt collector may not threaten you with legal action if you do not pay the debt. Implying or stating that legal proceedings will be undertaken when the right to pursue the debt has expired, may be coercive and misleading.

If you believe that a debt you owe may be statute-barred, you may wish to contact us.

Julie received a phone call from a debt collector at 7am on Saturday demanding that she pay up an old credit card debt. The debt collector has been to her house six times in the past week and threatened to report her to the Department of Communities: Child Protection and Family Support (CPFS) if she did not pay up.

Julie rang CCLS because she could not afford to pay the debt in full and was also afraid of being reported to the CPFS. CCLS advised Julie the debt collector breached the Debt Collection Guideline by calling before 9am on a weekend, by making contact more than 3 times in one week, and by their threat. CCLS also advised Julie about her rights and how she could make a complaint about the debt collector’s conduct.

Information on our website is provided for information only and is not legal advice. If you would like legal advice, please message us using the form below for a confidential discussion, or scroll down to see other ways to reach us.

If you would like further advice, please message us using the form below for a confidential discussion, or scroll down to see other ways to reach us.

{kind=link}